New Approaches to Support Energy Efficiency Investments

Introduction

CBEI joined the Pennsylvania Public Utility Commission’s On-Bill Financing (OBF) Working Group to consult on the potential application of this new form of financing for energy efficiency in the region’s building stock.

Despite the advantages of energy efficiency measures, the often high up-front costs of retrofitting remains a challenge for many commercial and residential customers. Financing energy efficiency interventions using conventional credit channels is often difficult for small commercial businesses and multifamily building owners. Underdeveloped underwriting standards within lending institutions, inappropriate use of payback calculations, and uncertainty surrounding the interventions themselves, among other reasons, contribute to this difficulty. Additionally, building and business owners must often weigh energy efficiency investments against other capital expenditures, slowing investment across the field. OBF is a way of overcoming these hurdles to make financing of energy efficiency measures accessible.

OBF “generally refers to a financial product that is serviced by, or in partnership with, a utility company for energy efficiency improvements in a building, and repaid by the building owner on his or her monthly utility bill,” according to a recent report by the American Council for an Energy Efficient Economy (ACEEE) [1]. Programs, which can be tailored to a particular sector (industrial, commercial, or residential), are typically structured to be “bill-neutral,” meaning that the payback from the energy savings is sufficient to ensure the customer sees no increase on their monthly utility bill.

PA Act 129 and On-Bill Financing

The OBF Working Group was created as part of Phase II of PA Act 129, an amendment to the Public Utility Code adopted in 2008 by the Pennsylvania General Assembly. PA Act 129 requires Pennsylvania’s seven largest electric distribution companies (EDCs) to develop energy efficiency and conservation plans and to adopt other methods of reducing the amount of electricity consumed by customers. The working group was charged with the task of investigating best practices from other states, assessing the feasibility of including OBF and repayment programs in Pennsylvania, and identifying potential options for customers to obtain low-cost financing for energy efficiency projects [2].

At a Working Group meeting held at the CBEI’s former Navy Yard headquarters (Building 101) on May 17, 2013, Deane Evans, from the New Jersey Institute of Technology, and CBEI former Deputy Director Laurie Actman gave an overview of CBEI role in advancing this initiative. CBEI is assisting the Working Group to design the program and provides the group with research, survey, and market analytics support. CBEI will conduct a deeper review of national on-bill financing programs, conduct a market assessment on key impact measures, and supply in-Hub quantitative analytics capability in support of the on-bill financing program design and test variables of the program, such as loan terms, interest rates, bill-neutrality, and cost impacts.

Understanding On-Bill Financing

OBF refers to a diverse range of programs that share the goal of using energy bills as a financial collection mechanism in order to spur investment in energy efficiency initiatives. Each OBF program must be adapted to the unique legal and regulatory frameworks of the region in which it is applied. OBF programs can be administered by a diversity of entities, including utilities, energy service companies (ESCO), nonprofit organizations, and in some cases, Community Development Financial Institutions (CDFI) or financial services providers [3].

OBF programs allow customers to pay for insulation, lighting, new heating systems, or other efficiency measures over extended terms in their monthly utility bill, structured as a service charge [1]. These programs leverage the unique existing relationship between the energy customer and the utility to provide convenient access to funding, especially for typically underserved segments of the market, such as rental and multifamily buildings.

The modified underwriting employed in OBF programs takes into account bill payment history, creating the potential for traditionally credit-constrained customers to gain access to financing. Because customers tend to prioritize their utility bill payments, default rates on OBF programs average less than 2 percent. Such low default rates have the potential to attract third-party lenders, indicating a high potential for scalability [3].

While in theory OBF could be made available across all markets of the building sector, the majority of existing programs target small businesses and homeowners, although a greater emphasis targeting multifamily households is a recent trend. OBF programs are evolving to suit a number of multifamily markets and to combat well-documented issues regarding split incentives [RD Report].

Loans and Tariffs

OBF mechanisms can typically be divided into two categories: loans and tariffs. Although the definition of loans and tariffs varies by state and locality, typically an on-bill loan program is a non-transferrable financial arrangement between a lending body, which provides the lump sum of funding to be repaid with interest, and a borrower (either a person or company) to finance an energy efficiency upgrade. By contrast, an on-bill tariff is a charge for energy efficiency upgrades that is transferrable and attached to the property; usually to a specific utility meter (a single property may have multiple meters).

Typically, a loan must be paid off either over time or when the property is sold. In some cases a loan will follow the initiating borrower post-sale. Because a tariff is attached to a property and not an individual or organization it can be transferred to subsequent owners.

According to ACEEE, loan programs are most often administered to small commercial and industrial customers; although programs for residential customers do exist, they are less common primarily as a result of complex consumer lending laws and utility companies’ reticence to act as a financial institution. In some states, utilities are even prohibited by law from providing loans to their customers.

A tariff, by contrast, can refer to any number of rates or charges imposed by a utility, including the price you pay per kilowatt-hour for your usage, generation and production, and transmission. In many states, on-bill tariffs are not considered loans and thus are subject to different laws and regulations [1]. On-bill tariffs leverage the existing fee-for-service financial arrangement between a utility and a client to finance energy efficiency investments or upgrades provided by the utility.

Funding On-Bill Programs

The seed capital to fund many existing on-bill financing programs came from revolving loan funds that were created using American Recovery and Reinvestment Act of 2009 (ARRA) [1]. Presently, the majority of current programs are still reliant on federal funding source (grants or loans) and/or ratepayer funds (the payback on existing lending) for capital.

The private sector is likely to be critical to the sustainability, growth, and scaling of these programs in the future. Private sector investors are more capable of securing sustained capital flow to fund this type of programs than government agencies or non-profits, which are reliant on funding that is far less secure. Utility, nonprofit, and ESCO-run programs can do more to attract third-party financiers by setting up loan loss reserves or loan guarantees [3].

Other than programs seeded by federal funding, utilities also finance on-bill programs through Community Development Financial Institutions and by leveraging government loans through agencies like the USDA’s Rural Utility Service.

Challenges of Changing the System

The nation’s energy efficiency needs will not be solved by OBF alone, nor is OBF appropriate in every situation. While OBF shows great promise in some scenarios, challenges remain and participation rates for existing programs have been far less than hoped for, usually below 0.5 percent of customers [1].

Low participation rates could stem from the perception that if financing measures are attached to meters in multi-family houses, property owners could bear the risk of repayment if they encounter difficulty in filling vacancies. This problem could be addressed through program design or legislation, however. In rental markets, using clear legal language to define whether landlords or tenants are responsible for repayment is important. Which party appropriately bears responsibility will vary market to market depending on how utilities are distributed at the majority of rental properties, and how billing is handled by the utility. Ensuring that tenants who are responsible for repayment are notified and accept the responsibility prior to signing a new lease is also important [3].

The difficulty of calculating and guaranteeing exact energy savings – caused by the multiplicity of factors that determine energy use – constitutes another challenge. To address this, some programs mandate audits either before or after the intervention, or both, to ensure that a measurable energy savings has been achieved and to increase consumer confidence.

The structure of OBF programs generally steers customers towards short-term solutions in order to preserve bill-neutrality rather than encouraging them to pursue deep retrofits. Whether or not bill neutrality is an absolute requirement for a successful program is debated in the field. While bill-neutrality increases the likelihood that a customer will be able to meet the financial obligation of repayment, it may also inhibit the potential for owners to undertake advanced energy retrofits , as well as inhibiting the lender’s financial gain from lending for larger projects [3].

Even with bill-neutrality, there is some risk that customers might fall upon hard times and be subject to utility disconnection or default [3]. Creating credit enhancements (loan-loss reserves or payment guarantees from public benefit funds) can spread the risk of non-payment.

Utilities have also expressed concern about the upfront costs of modifying their billing systems to accommodate these programs. Utilities perceive that they must function as a financial institution to participate in on-bill financing, which would require the utilities to become compliant with complex consumer lending practices, a costly investment of manpower, time, and money. Law-making bodies must alleviate this perception by clearly laying out the utilities’ responsibilities.

On-Bill Financing Programs

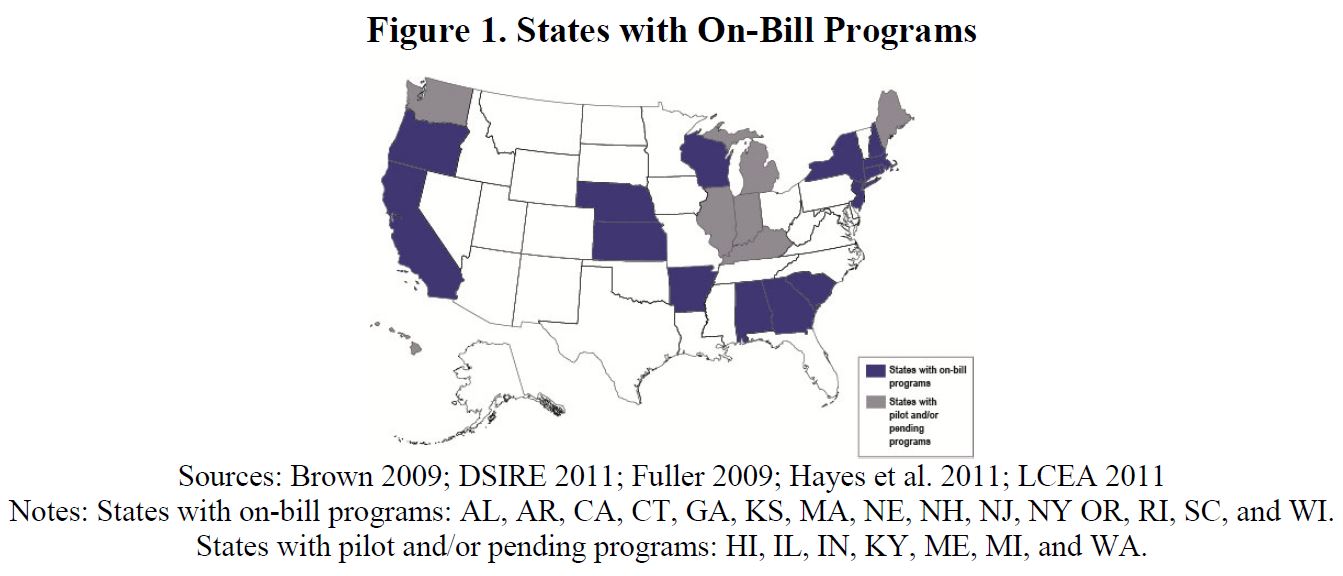

Currently, utilities in at least twenty-two states have implemented or soon will implement OBF programs. Many of the states with such utilities (Illinois, Hawaii, Oregon, California, Kentucky, Georgia, South Carolina, Michigan, and New York) have legislation in place that supports OBF adoption in various ways. Some states, such as Illinois and California, require utilities to implement on-bill programs. Other states remove barriers to implementation by allowing for a tariff for energy efficiency services or for financing to be collected through utility billing. New York state’s OBF legislation allocated the funds to update the billing systems for utilities that offer OBF programs.

Additionally, a number of utility regulators in states without existing programs have taken action to explore the feasibility of on-bill programs. Pennsylvania is currently in the process of developing a pilot program for on-bill financing. The model under discussion, proposed by the Sustainable Energy Fund, would be limited to small commercial and industrial businesses [4].

References:

[1] Bell, Catherine J., Nadel, Steven, and Sara Hayes. (2011). “On-Bill Financing for Energy Efficiency Improvements: A Review of Current Program Challenges, Opportunities, and Best Practices.” ACEEE, from http://www.puc.state.pa.us/Electric/pdf/Act129/OBF-ACEEE_OBF_EE_Improvements.pdf

[2] “On-Bill Financing Working Group”. Pennsylvania Public Utility Commission, from http://www.puc.state.pa.us/filing_resources/issues_laws_regulations/act_129_information/on_bill_financing_wg.aspx

[3] Bell, Catherine J., and Steven Nadel. “On-Bill Financing: Exploring the Energy Efficiency Opportunities and Diversity of Approaches.” ACEEE, from http://www.puc.state.pa.us/Electric/pdf/Act129/OBF-ACEEE_OBF_Exploring_EE_Opps-Approaches.pdf

[4] Costlow, J. (2012). “On-Bill Repayment: Model for Pennsylvania.” Sustainable Energy Fund, from http://www.puc.state.pa.us/Electric/docs/Act129/OBF-PA_OnBill_Repayment_Program.docx